Dear friends,

in the link here-below you find the latest estimation for the production crop 2017 as well as final number report for crop 2016 which at the end was a little higher than first indication:

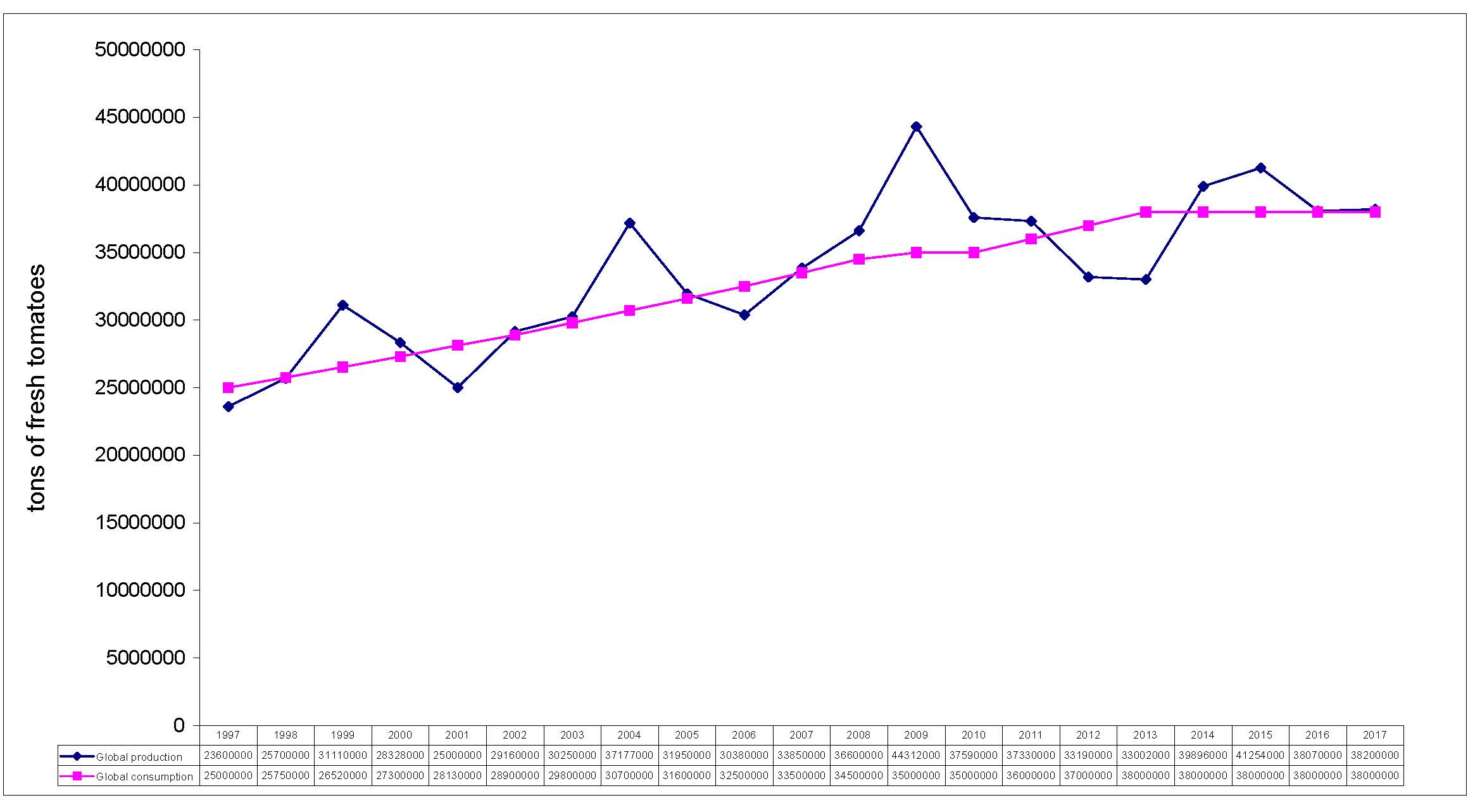

world production estimate 2017

We are calculating a steady global consumption since 2013 around a quantity of 38 millions tons fresh tomatoes equivalent.

For years consumption was increasing quite sharply but in the last years we have noticed a different trend probably connected by a number of factors such as:

See below the graph which is resuming the position of global production and consumption trend.

We are starting the new season with some carryover present above all in California, in a lower extent in China and in Europe.

All together, also considering that production forecast is matching global demand, we were starting negotiation pre-season in a good condition and we were expecting prices remaining more or less in the range of last year. On the contrary we have noticed above all from Europe very aggressive quotations in the range of 10-15% lower than pre-season crop 2016.

Business crop 2017 have been concluded in the following range:

Carryover crop 2016 available for deal at discount to be agreed.

At the above prices we are often below production costs and what is really worrying is that this movement is not finding a logic justification in the current market situation.

In the past the reduction of the market price was connected to an excess of carryover and/or expectation of a very large production (see crop 2009 from the above graph).

Today this negative trend is probably more connected to the financial weakness of too many producers.

If this is the logic only chance is a lower global production but I cannot see this is coming from a reduced planning also because the largest producers such as California and China are already packing well below the installed capacity.

So only help may come by some adverse weather condition and this is not a good news !

Have a nice crop!

Armando Gandolfi