We have just attended the WPTC meeting held in Chile and we have now available a first detailed forecast for the production crop 2016.

From the below link in red , you will find a document (more accurate forecast to be confirmed around end of June) where you can see that the global quantity should be equivalent to 39,392,000 tons of fresh tomatoes and, if confirmed, this is about 5% below the final number of crop 2015.

WPTC World Production estimate as of 6 March 2016

We must also highlight that nearly all reduction is coming from California where a major drop in the production has been decided above all in connection to the strong USD rate which, of course, has limited their competitiveness in the market.

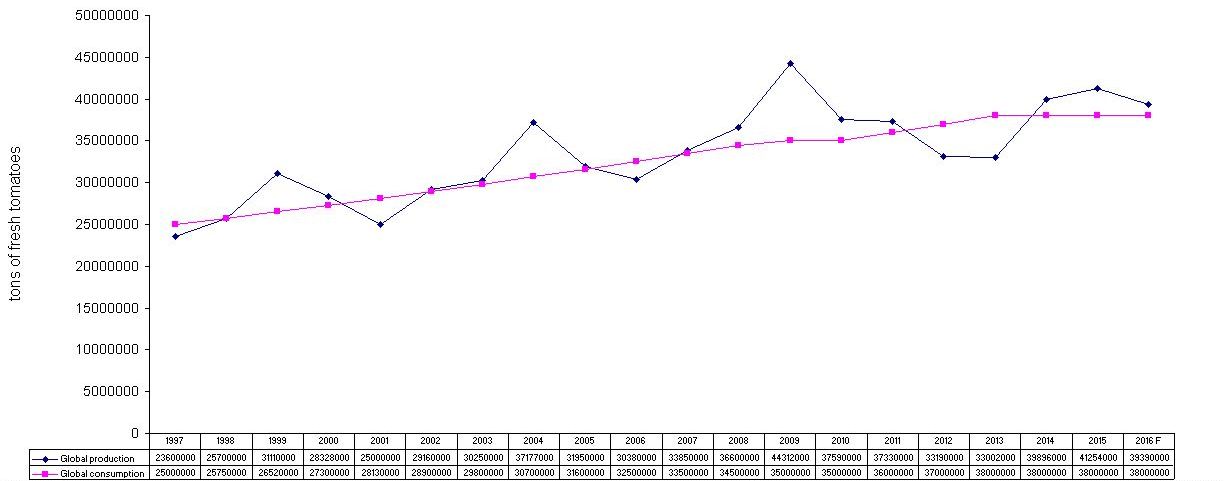

We think it is very interesting to cross the data of the production with those of the consumption and from the below graph it looks evident how, different from the past, carryovers available are and probably will always be very limited. The reason of this change of trend is that in the past China was, thanks to the very low production costs, very aggressive and pushing to increase strongly its production but this is no longer the case.

China, whose production costs increased substantially, has been forced to change its commercial strategy and this new approach is well reflected in the attached document.

In spite the fact that most of the carryover at the start of crop 2016 will be available in California, our forecast is that the market will remain quite weak also in Europe and China. The reason is not caused by any over production forecast but by the structural and financial weakness of too many and often too small producers.

Useless to say that change of market trends are becoming more easy in case of adverse weather conditions because the difference between consumption and production is now only about 3.5% that is a very small percentage for an agricultural product !

Coming back to the consumption a great concern is coming from regional important crisis mainly caused by the very low oil price and/or local wars potentially affecting consumption of important consumers such as Libya, Nigeria and others.

This is why in spite the increase of population since some years we keep flat the consumption at a rate of 38,000,000 tons fresh tomatoes equivalent while the official statistics are suggesting a number closer to 40,000,000.

About the fresh tomato price and just limiting the information to main producing countries:

As you can see from the above as short resuming lower production but lower production costs.

At this point our personal suggestion is to watch carefully the development of the planting situation during the springtime before taking any position.

For this reason we will report updated information around the end of May/begin of June.

Keep in touch